All Categories

Featured

Table of Contents

- – What does a basic Trust Planning plan include?

- – Is Cash Value Plans worth it?

- – Is Trust Planning worth it?

- – What should I know before getting Wealth Tran...

- – What are the benefits of Accidental Death?

- – What types of Mortgage Protection are availa...

- – What should I look for in a Legacy Planning ...

- – What is the difference between Long Term Car...

- – What is Guaranteed Benefits?

Juvenile insurance policy might be sold with a payor benefit motorcyclist, which offers waiving future costs on the kid's plan in case of the fatality of the person who pays the premium. Senior life insurance coverage, in some cases referred to as graded survivor benefit plans, supplies eligible older applicants with very little entire life protection without a medical exam.

These plans are generally more expensive than a completely underwritten policy if the individual certifies as a conventional risk. This kind of insurance coverage is for a little face amount, generally bought to pay the interment expenses of the guaranteed.

This implies they can pay a component of the policy's survivor benefit while you're still active. These policies can be an economic resource you can make use of if you're identified with a covered ailment that's thought about chronic, important, or terminal. Life insurance policy plans fall into 2 classifications: term and permanent. A term life insurance policy offers you protection for an established variety of years.

In addition, a portion of the costs you pay into your entire life policy constructs cash worth over time. Some insurance companies use tiny entire life plans, typically referred to as.

What does a basic Trust Planning plan include?

Today, the cost of a typical term life insurance for a healthy and balanced 30-year-old is approximated to be around $160 per year simply $13 a month. 1While there are a great deal of variables when it concerns just how much you'll spend for life insurance coverage (plan kind, advantage quantity, your profession, etc), a plan is most likely to be a great deal less costly the more youthful and much healthier you are at the time you buy it.

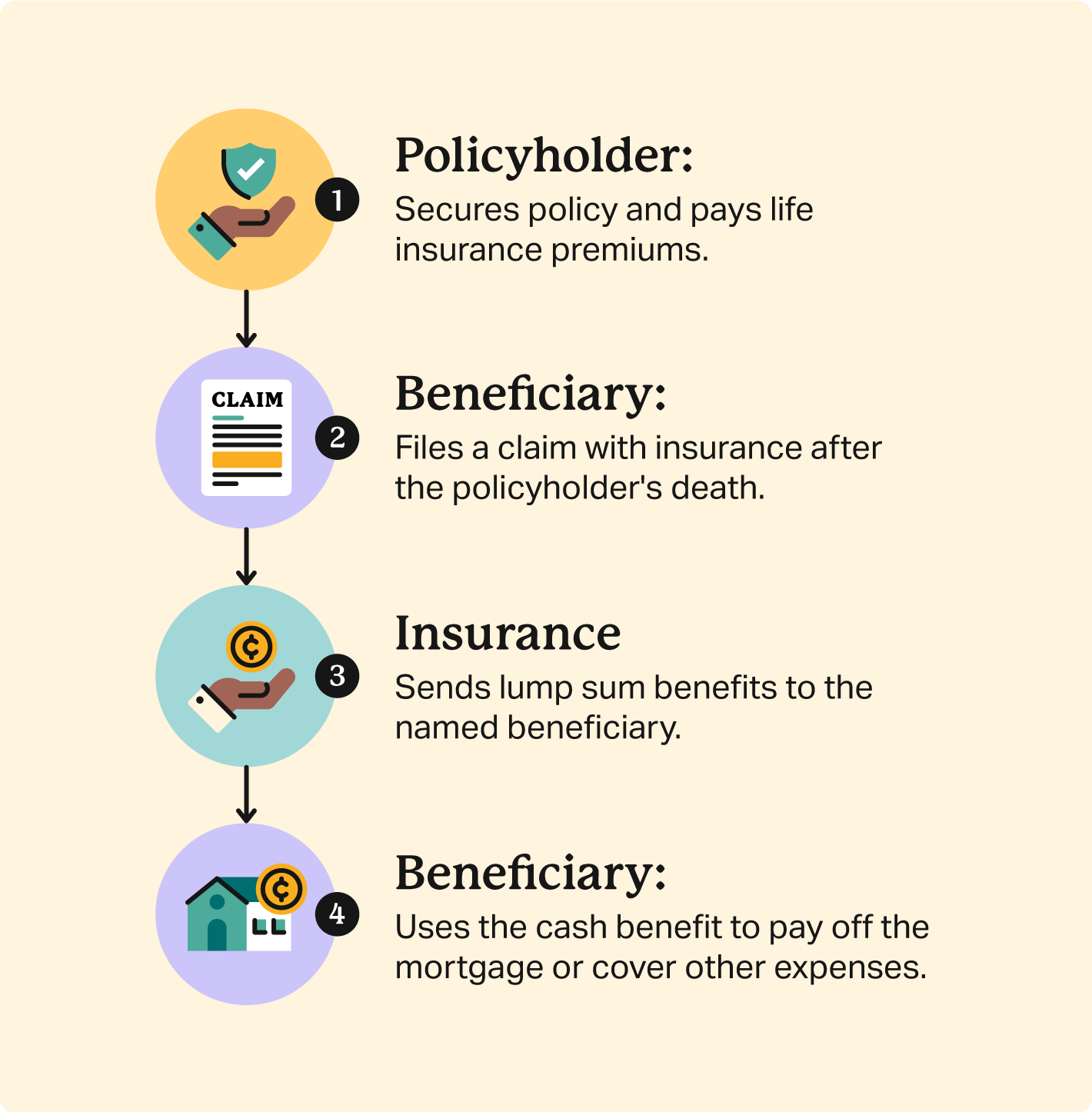

Beneficiaries can typically obtain their cash by check or digital transfer. On top of that, they can additionally select just how much cash to obtain. As an example, they can get all the cash as a lump amount, using an installation or annuity plan, or a retained asset account (where the insurance provider acts as the financial institution and allows a beneficiary to create checks against the equilibrium).3 Free Mutual, we understand that the choice to get life insurance policy is an important one.

Is Cash Value Plans worth it?

Every effort has been made to ensure this information is existing and right. Information on this web page does not ensure registration, advantages and/or the ability to make modifications to your advantages.

Age reduction will apply during the pay duration having the covered person's applicable birthday celebration. VGTLI Age Decrease Age of Worker Amount of Insurance Policy 65 65% 70 40% 75 28% 80 20% Beneficiaries are the person(s) assigned to be paid life insurance policy advantages upon your death. Recipients for VGTLI are the same as for GTLI.

Is Trust Planning worth it?

This benefit may be continued up until age 70. You have 30 days from your retired life day to choose this insurance coverage making use of one of the two alternatives below.

Succeeding quarterly premiums in the amount of $69 are due on the first day of the following months: January, April, July and October. A premium due notice will certainly be sent to you around 30 days prior to the next due day.

You have the option to pay online making use of an eCheck or credit/debit card. Please note that solution costs might use. You additionally have the alternative to mail a check or money order to the listed below address: The Ohio State UniversityAccounts ReceivablePO Box 182905Columbus, OH 43218-2905 Costs prices for this program go through change.

Premium quantities are figured out by and paid to the life insurance vendor.

What should I know before getting Wealth Transfer Plans?

If you retire after age 70, you may convert your GTLI protection to an individual life insurance coverage policy (up to $200,000 optimum). Premium quantities are established by and paid to the life insurance coverage supplier.

The benefit quantity is based on your years of work in an eligible appointment at the time of retired life and is payable to your recipient(-ies) as complies with: $2,000 $3,000 $4,000 $5,000 This is intended to be a summary. In the occasion the info on these pages differs from the Plan Document, the Plan File will govern.

Term life insurance plans expire after a specific number of years. Long-term life insurance policy policies continue to be active till the insured person passes away, stops paying premiums, or gives up the plan. A life insurance coverage plan is just as good as the economic strength of the life insurance coverage business that releases it.

Some policies enable automated superior finances when a premium settlement is overdue. is one type of irreversible life insurance policy where the premium and survivor benefit normally remain the very same every year. It includes a cash money value part, which resembles a financial savings account. Cash-value life insurance policy allows the insurance holder to make use of the cash worth for many purposes, such as to obtain car loans or to pay plan premiums. Complete what these costs would certainly be over the next 16 or so years, include a little much more for inflation, which's the death advantage you could wish to buyif you can manage it. Funeral or last expense insurance policy is a sort of permanent life insurance that has a tiny survivor benefit.

What are the benefits of Accidental Death?

Numerous factors can affect the price of life insurance policy premiums. Particular things might be past your control, but other requirements can be managed to potentially lower the expense prior to (and also after) applying. Your health and age are one of the most essential factors that determine price, so buying life insurance policy as quickly as you need it is typically the most effective strategy.

If you're found to be in far better wellness, after that your premiums might decrease. You may also have the ability to get extra protection at a reduced rate than you initially did. Investopedia/ Lara Antal Think of what costs would require to be covered in case of your death. Take into consideration things such as home loan, university tuition, bank card, and various other debts, as well as funeral service expenditures.

There are valuable tools online to determine the round figure that can satisfy any type of prospective expenses that would certainly need to be covered. Life insurance coverage applications usually call for individual and family medical background and beneficiary information. You may need to take a medical examination and will require to divulge any kind of pre-existing medical problems, background of moving infractions, Drunk drivings, and any hazardous hobbies (such as automobile racing or skydiving).

Since women statistically live much longer, they usually pay lower prices than men of the same age. An individual who smokes is at risk for lots of health and wellness issues that might reduce life and rise risk-based premiums. Medical examinations for most policies include screening for health problems such as heart problem, diabetic issues, and cancer cells, plus associated medical metrics that can indicate health and wellness risks.: Hazardous line of work and leisure activities can make costs a lot more pricey.

What types of Mortgage Protection are available?

A background of moving offenses or dwi can drastically boost the price of life insurance policy costs. Typical forms of recognition will certainly also be required before a plan can be composed, such as your Social Protection card, vehicle driver's license, or U.S. passport. Once you have actually assembled all of your required info, you can collect multiple life insurance policy quotes from different suppliers based upon your research study.

Since life insurance policy costs are something you will likely pay month-to-month for decades, discovering the policy that finest fits your requirements can save you an enormous quantity of cash. Our schedule of the finest life insurance business can offer you a jump start on your research study. It details the business we've located to be the very best for various sorts of requirements, based on our study of nearly 100 providers.

Below are a few of one of the most important features and protections provided by life insurance policy policies. Most individuals utilize life insurance policy to provide cash to beneficiaries that would certainly endure financial challenge upon the insured's death. for affluent people, the tax advantages of life insurance coverage, including the tax-deferred growth of cash value, tax-free rewards, and tax-free survivor benefit, can give extra strategic possibilities.

, however that's why affluent individuals often buy irreversible life insurance coverage within a trust., which is illegal.

What should I look for in a Legacy Planning plan?

Married or not, if the fatality of one grownup could imply that the various other can no more afford funding settlements, upkeep, and tax obligations on the property, life insurance policy may be an excellent idea. One example would be an engaged pair that get a joint home loan to get their very first residence.

:max_bytes(150000):strip_icc()/dotdash-variable_universal-Final-66a32d4c8d84418ab1271e02d73d2a4b.jpg)

This help might likewise consist of straight financial support. Life insurance can aid reimburse the adult kid's costs when the parent passes away - Mortgage protection. Young person without dependents hardly ever need life insurance policy, but if a parent will certainly get on the hook for a kid's debt after their fatality, the child might desire to lug enough life insurance coverage to repay that debt

A 20-something adult could purchase a plan even without having dependents if they anticipate to have them in the future. Stay-at-home spouses must live insurance as they add considerable economic worth based on the job they do in the home. According to, the financial value of a stay-at-home moms and dad would certainly amount an annual salary of $184,820.

'A little life insurance coverage plan can supply funds to honor a loved one's death. If the death of a vital employee, such as a CHIEF EXECUTIVE OFFICER, would produce severe economic challenge for a firm, that service may have an insurable passion that will certainly allow it to acquire a key person life insurance coverage plan on that worker.

What is the difference between Long Term Care and other options?

Each policy is one-of-a-kind to the insured and insurer. It's vital to examine your policy file to comprehend what risks your policy covers, just how much it will certainly pay your recipients, and under what conditions.

That security matters, considered that your successors may not obtain the death benefit up until several decades into the future. Investopedia has evaluated scores of companies that provide all different sorts of insurance and ranked the ideal in numerous groups. Life insurance policy can be a prudent economic tool to hedge your wagers and provide security for your liked ones in instance you die while the policy is in pressure.

What costs could not be met if you died? It is still vital to think about the influence of your possible fatality on a partner and think about just how much financial support they would certainly need to grieve without worrying regarding returning to work before they're ready.

If you're purchasing a plan on another family members member's life, it is necessary to ask: what are you trying to insure? Children and elders truly do not have any type of meaningful income to replace, yet funeral costs may require to be covered in case of their death. Furthermore, a parent might intend to protect their kid's future insurability by purchasing a moderate-sized policy while they are young.

What is Guaranteed Benefits?

Term life insurance policy has both components, while irreversible and whole life insurance plans also have a money value element. The survivor benefit or stated value is the amount of money the insurance provider assures to the beneficiaries determined in the policy when the insured passes away. The guaranteed may be a parent and the beneficiaries may be their youngsters, for instance.

Premiums are the money the insurance policy holder pays for insurance policy.

{kind=link}

Table of Contents

- – What does a basic Trust Planning plan include?

- – Is Cash Value Plans worth it?

- – Is Trust Planning worth it?

- – What should I know before getting Wealth Tran...

- – What are the benefits of Accidental Death?

- – What types of Mortgage Protection are availa...

- – What should I look for in a Legacy Planning ...

- – What is the difference between Long Term Car...

- – What is Guaranteed Benefits?

Latest Posts

Life Insurance Expenses

Final Expense Insurance Agencies

Best Final Expense Carriers

More

Latest Posts

Life Insurance Expenses

Final Expense Insurance Agencies

Best Final Expense Carriers